{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Volatility in Agricultural Prices (Ebook available for Download)

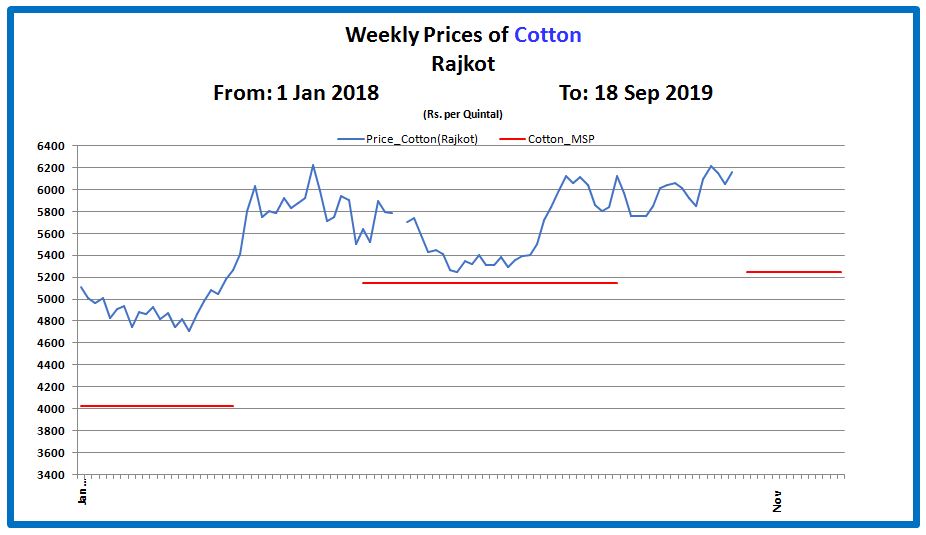

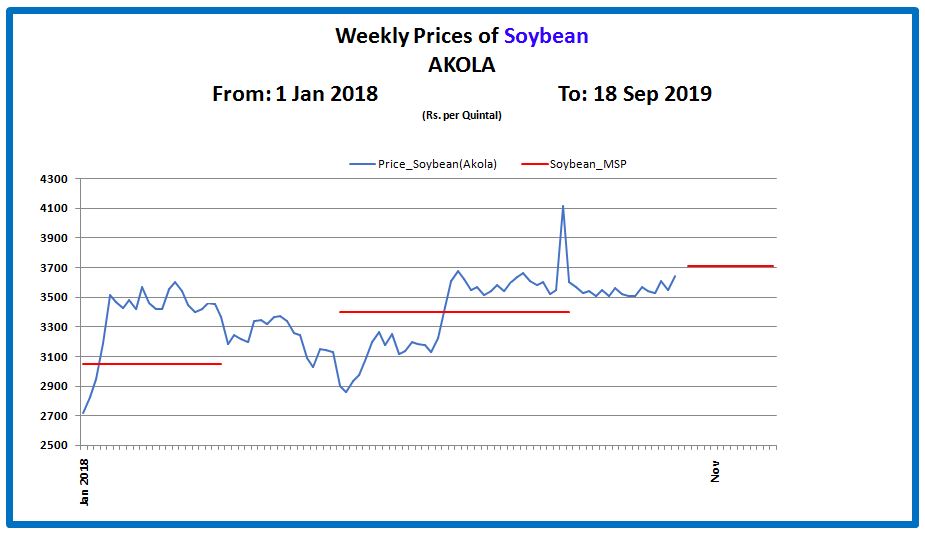

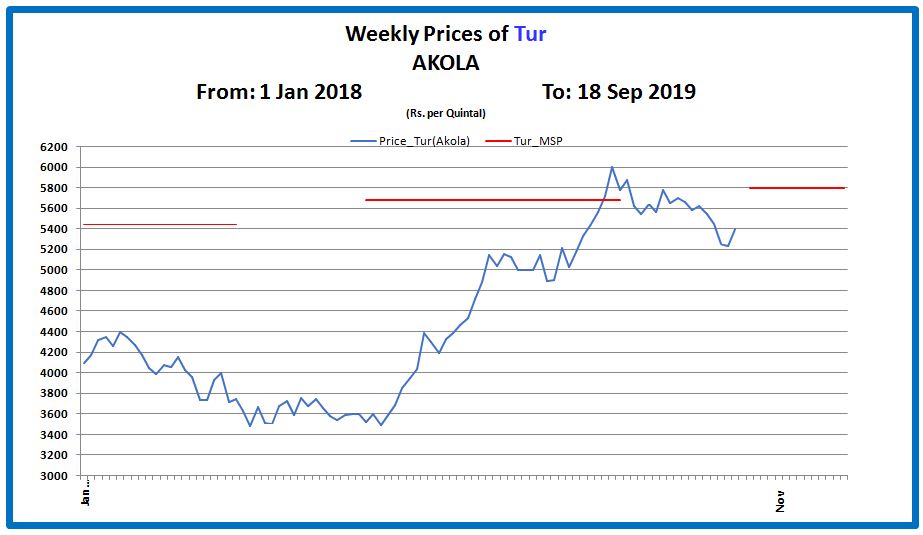

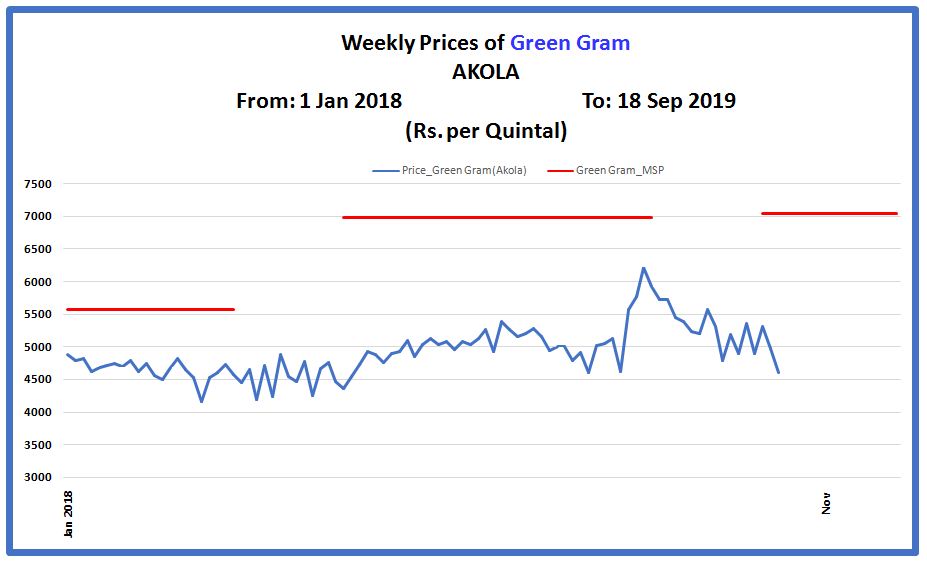

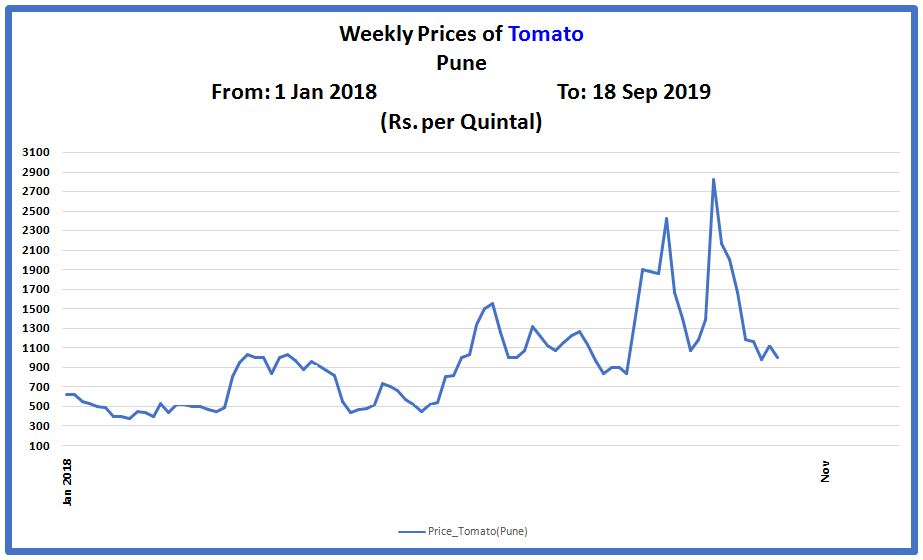

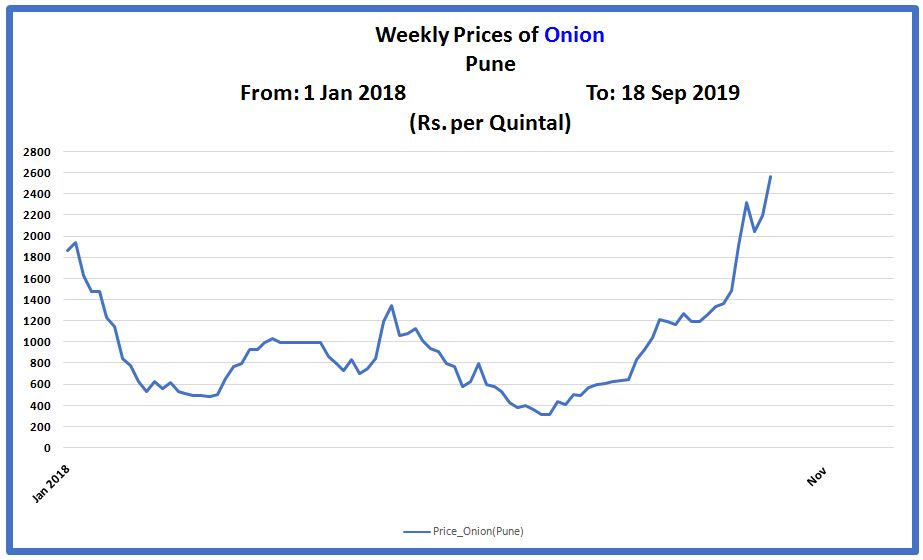

Volatility in agricultural prices has been a subject of concern not only for India but also for several developing and developed countries in the 21stcentury. The present study attempts to measure and compare volatility in monthly prices of 84 agricultural commodities during the period of 37 years between April 1982 and March 2019.

For the sake of comparison, this period is divided into three sub-periods. The data used are the Wholesale Price Indices for individual commodities published by the Office of the Economic Adviser, Department for Promotion of Industry and Internal Trade, Government of India.

Three components of price fluctuations are examined. One, which is caused by seasonality in supply, another that is the result of secular the trend in prices and the remaining component of other fluctuations (cyclical and irregular).

The presence and extent of seasonality are estimated by using X-13ARIMA-SEATS methodology developed by the U. S. Department of Commerce, U. S. Census Bureau. The trend is estimated from the deseasonalized series by calculating the annual compound growth rates in the series in both nominal and real terms.

Volatility is measured by calculating the coefficient of variation of the original series as also of the residual series (after removing seasonality and trend). Seasonality, trend and volatility are calculated for each commodity and each sub-period.

To know more in detail, kindly refer our published E-book for this subject.

Executive Summary-Volatility in Agricultural Prices

Send download link to:

Volatility in Agricultural Prices

Send download link to: